John, CPA, is auditing the financial statements of ABC Bank Co.for the year ended December 31,20×8. The following information is available:(a)John assessed the risk of material misstatements in short-term loan account at 80% and plans to limit to 10% the risk of failing to detect misstatements in the account equal to the tolerable error assigned to the account.(b) John is testing the operating effectiveness of the loan approval procedure(a control activ- ity) related to granting loans. In 20×8,ABC Bank granted to 10 000 loans in total. John deter- mined that the acceptable risk of assessing control risk too low is 10%. He selected a sample made up of 60 sampling units and tested without any deviation found. Some Poisson Risk Factors(Relia- bility Factors) are reprinted as follows:(c) John is using the Ratio Estimation Variable Sampling method to test the long-term loan balance at December 31, 20×8. The total recorded balance is RMB¥300 billion , made up of 4 000 items. John designed a sample made up of 200 items . The book value of the sample is RMB¥16. 5 billion. However, the audited value is RMB¥15. 6 billion.(d) John is performing substantive procedures on interest income from short-term loan. The average annual market interest rate for short-term loan is 5 percent. The audited short-term loan balances of ABC Bank Co. at the end of each month in 20×8 are as follows:Required :(1) Based on (a) , calculate the acceptable detection risk.(2) Based on (b) , calculate the upper limit of population deviation rate.(3) Based on (c), make a point estimate of the misstatement in the population. Sampling error need not to be considered.(4) Based on (d) , develop the expected result of interest income from short-term loan.(5) Assume that after the tests mentioned in (d) , John found that the interest income from short-term loan was understated by RMB¥0. 05billion. Prepare the adjusting entry.

John, CPA, is auditing the financial statements of ABC Bank Co.for the year ended December 31,20×8. The following information is available:

(a)John assessed the risk of material misstatements in short-term loan account at 80% and plans to limit to 10% the risk of failing to detect misstatements in the account equal to the tolerable error assigned to the account.

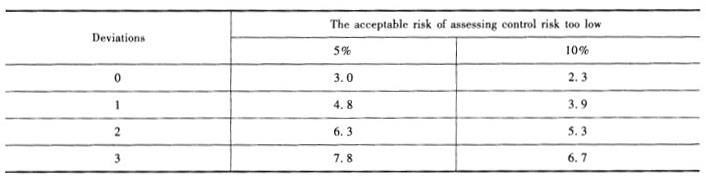

(b) John is testing the operating effectiveness of the loan approval procedure(a control activ- ity) related to granting loans. In 20×8,ABC Bank granted to 10 000 loans in total. John deter- mined that the acceptable risk of assessing control risk too low is 10%. He selected a sample made up of 60 sampling units and tested without any deviation found. Some Poisson Risk Factors(Relia- bility Factors) are reprinted as follows:

(c) John is using the Ratio Estimation Variable Sampling method to test the long-term loan balance at December 31, 20×8. The total recorded balance is RMB¥300 billion , made up of 4 000 items. John designed a sample made up of 200 items . The book value of the sample is RMB¥16. 5 billion. However, the audited value is RMB¥15. 6 billion.

(d) John is performing substantive procedures on interest income from short-term loan. The average annual market interest rate for short-term loan is 5 percent. The audited short-term loan balances of ABC Bank Co. at the end of each month in 20×8 are as follows:

Required :

(1) Based on (a) , calculate the acceptable detection risk.

(2) Based on (b) , calculate the upper limit of population deviation rate.

(3) Based on (c), make a point estimate of the misstatement in the population. Sampling error need not to be considered.

(4) Based on (d) , develop the expected result of interest income from short-term loan.

(5) Assume that after the tests mentioned in (d) , John found that the interest income from short-term loan was understated by RMB¥0. 05billion. Prepare the adjusting entry.

参考解析

(1) acceptable detection risk = audit risk/the risk of material misstatement s = 10%/80% = 12. 5%

(2) The upper limit of population deviation rate = Poisson risk factor/sample size = 2. 3/60 = 3. 83 %

(3) ratio = 156/165 = 94. 54%

estimate the actual value of the population = 3 000*94. 54% = 283. 62 billion a point estimate of the misstatement in of the population =3 000 -283. 62 *10 = 16. 38 billion

(4) the expected result of interest income from short-term loan = (300 +320 +310 +300 + 330 +320 +320 +290 +310 +330 +300 +290)*5% =18. 6 billion

(5) the adjusting accounting entry:

Dr: Interest suspense 156

Cr: Interest income 156